PRMIA 8008 Question Answer

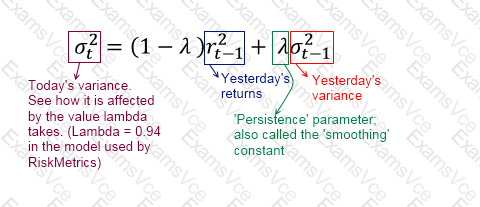

A stock's volatility under EWMA is estimated at 3.5% on a day its price is $10. The next day, the price moves to $11. What is the EWMA estimate of the volatility the next day? Assume the persistence parameter λ = 0.93.

PRMIA 8008 Summary

- Vendor: PRMIA

- Product: 8008

- Update on: Aug 4, 2026

- Questions: 362